The NEC4 Professional Service Contract launched in 2017 broke the norm of paying consultants tendered rates for their staff. Instead, in NEC4 PSC options C and E (target cost and cost reimbursable), consultants are paid the real costs of employing their staff. This mimics what has been the case for contractors under cost-based options of the NEC3 Engineering and Construction Contract (ECC) since 2005.

Indeed, one of the drivers in the upgrade from NEC3 to NEC4 was to bring the various NEC contracts together when there was no reason for them to be different. Here NEC has effectively said, ‘why should we treat consultants differently?’ The result is that the NEC4 PSC may be the only standard form of consultancy contract where this is the case. This article explains how the contract works and looks at the pros and cons of the change. It also explains how a client could choose to stick with a rates-based approach.

Payment under NEC4 PSC

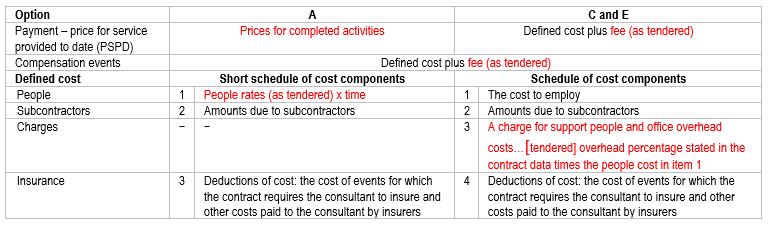

For NEC clients adopting the NEC4 PSC options C or E for the first time, the change in the payment mechanism will probably be the most significant thing they notice. NEC3 PSC used the concept of time charge, which was calculated simply as tendered staff rates multiplied by the time worked. That was used for assessing compensation events for all options − A (lump sum), C and E − and for routine payment for options C and E.

NEC4 PSC adopts the ECC concept of defined cost plus fee for assessing compensation events for all options and for routine payments in options C and E. The fee is calculated as the tendered fee percentage multiplied by the defined cost.

Clause 52.1 requires that any element of defined cost that is not set by a rate in the contract data is required to be, ‘at open market or competitively tendered prices with deductions for all discounts, rebates and taxes which can be recovered’. The way money is handled in NEC4 PSC is summarised in Table 1.

Option A

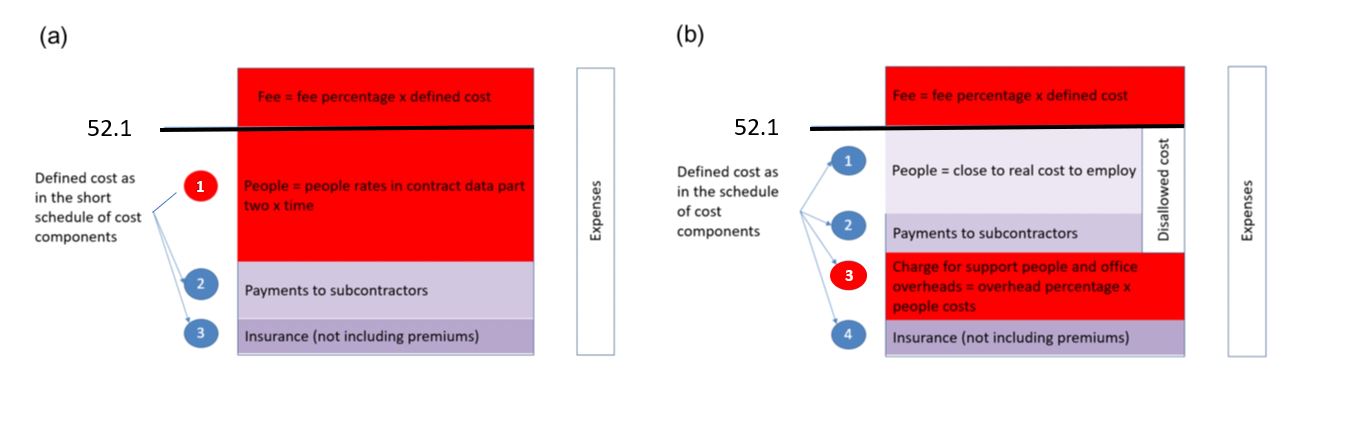

In NEC4 PSC option A, the routine payment is the prices of completed activities. Compensation events are assessed based on defined cost plus fee. Defined cost in option A is illustrated in Figure 1 (a).

Defined cost is set out in the short schedule of cost components (SSCC) and is made up primarily of people rates as tendered multiplied by the time worked, and payments made to subcontractors. If the client wants to allow any expenses they must state them in the contract data. As shown in Figure 1 (a), any such expenses are paid separately and are not subject to the fee percentage.

Compared with NEC3 PSC, we still have rates tendered for the consultant’s own people. The difference is that in NEC4 PSC these ‘people rates’ are subject to the fee percentage. In NEC3 PSC, actual payments to subcontractors (called subconsultants) could be paid only if listed as an ‘expense’ by the client in contract data part one. In NEC4 PSC the amount due to subcontractors is always part of defined cost.

When bidding, it is logical for the tenderer to set the fee percentage based on the mark-up they wish to receive on subcontractors. Then they will then set the people rates to ensure that their required mark-up on the real cost of people is achieved. This will have to consider whether and which expenses are allowed and the fact that the tendered people rates are subject to the fee percentage. However, any tenderer will need to take note of how the fee percentage and people rates are to be used by the client in tender evaluation.

Options C and E

In NEC4 PSC options C and E, the routine payment (as in ECC) is now based on defined cost plus fee. Clause 11.2 (21) states, ‘The Price for Service Provided to Date is the total Defined Cost which the Service Manager forecasts will have been paid by the Consultant before the next assessment date plus the Fee.’

In NEC3 PSC the consultant was paid the time charge already spent. NEC4 PSC copies the ECC process of paying what is forecast to be paid by the next assessment date. That forecast will be included in the consultant’s application for payment and then in the service manager’s assessment of the amount due. The reduced need for the consultant to finance the service should be reflected in the tendered fee percentage. However, there is an issue here.

Clause 50.1 has, ‘The first assessment date is decided by the Service Manager to suit the procedures of the Parties’. If they choose the day of the month the day before the consultant pays its staff, there will be no inclusion of next month’s forecast spend. If they choose the day of the month after the consultant pays its staff, the consultant will get the benefit of a full month’s advance payment. The problem is that decision is taken only after award. The consultant needs to know when this will be as it bids so it can allow for the level of ‘work in progress’ on its books and the financing costs involved.

All compensation events are also assessed based on defined cost plus fee. The only difference between options C and E is that option C has the target mechanism and the consultant’s share, which depends on how well the consultant does compared with the target total of the prices. The purpose of this is to encourage the client and consultant to collaborate and jointly manage risks and jointly reduce the defined cost during delivery of the service.

Defined cost in option C and E is as defined in the schedule of cost components (SCC) less disallowed cost and is illustrated in Figure 1 (b). It is made up primarily of payments for the consultant’s people based on something very close to the real cost of employing them, payments made to subcontractors, and a charge for ‘support people and office overhead costs’ calculated by applying the overhead percentage stated in the contract data to the total of people items 11, 12 and 13 of the SCC. As shown in Figure 1 (b), as for NEC4 PSC option A, if the client allows any expenses, they are paid separately and are not subject to the fee percentage.

Clause 52.3 (in NEC PSC options C and E, but not in option A) states, ‘The Consultant keeps these records… accounts of payments of Defined Cost and expenses, proof that the payments have been made, communications about and assessments of compensation events for Subcontractors and other records as stated in the Scope’ (bullets omitted).

One obvious record likely to be required, and needing to be stated in the scope, is the timesheets of employees and any subcontractor’s employees under a target or reimbursable subcontract. Clients are likely to want those timesheets to include details of the actual work being done.

Clause 52.4, the ‘open book’ clause, allows the service manager to access the records required to be kept. This may present a problem for the consultant, especially if the service manager (new to NEC4 PSC and carrying out a role similar to the project manager in ECC) is an employee of a competitor. The consultant is very likely at least to want to put a confidentiality agreement in place (this is not provided for in NEC4 PSC). The details of defined cost are set out in the SCC.

Defined cost in the SCC

People

The items in SCC 1 are very close to the real cost of employing a member of staff. But consultants will need to check for any differences in the NEC’s rules compared with how they themselves calculate and record the cost of their staff. For example, in Mott MacDonald, our ‘cost’ of an individual as booked to a project includes a small uplift to contribute to a corporate fund for (possible) redundancy payments. That cost is not part of the NEC’s defined cost, so will not be paid and have to be covered in a tendered percentage. Note that any actual redundancy costs on the contract are part of defined cost (SCC 12(c)).

SCC 11 includes, ‘A cost calculated by dividing the total of the following payments by the total time recorded, with the resulting amount multiplied by the time recorded for work on the contract. Time recorded is that shown in the Consultant’s time recording system.’ So, effectively on day one of the contract, the cost recoverable (effectively a rate) for each person will need be calculated based on the real cost of that person. This is unlike in option A, where the people rates are tendered.

If the cost of the individual changes, the cost will logically change. This is implicit in SCC 11, but there is no explicit mention of changes. It would be appropriate to include an explicit provision to revise the calculated rates after changes in salary or other employment conditions.

Note that the ‘total time recorded’ will include time for leave, bank holidays, sickness and non-billable time. The cost of leave and bank holidays is effectively included in the individual’s salary. The cost of other leave (e.g. sickness and jury service) and non-billable time could be included in the ‘overhead percentage for the cost of support people and office overheads’ or in the fee percentage.

SCC 13 includes as defined cost amounts paid for people not directly employed but who are paid according to the time spent on the work. That will include for example for contract staff, including those employed through a staff agency.

Subcontractors

SCC 2 is payments to subcontractors. Note that the client is protected by the provisions of clause 23 relating to the acceptance of subcontractors and the subcontracts including the ‘pricing information’ in those subcontracts which is submitted for information. So, payments to subcontractors should not come as a surprise.

Charges

SCC 3 states, ‘The following components of the cost of support people and office overhead... A charge for support people and office overhead costs calculated by applying the overhead percentage stated in the Contract Data to the total of people items 11, 12 and 13. The charge includes provision and use of people, accommodation, equipment, supplies and services required to provide the office and to support people providing the service.’

The contract data part two enables the client to allow the tenderer to state different overhead percentages for different locations. The preamble to the SCC makes it clear that an amount is included ‘only in one cost component’. Hence ‘support people’ are covered by the overhead, and so not directly paid under SCC 1. This will include accounting staff and other staff normally considered an overhead. To avoid potential disputes over the intended coverage of this charge, clients may want to make clearer in the contract the staff intended to be covered by the overhead percentage and so not directly billable under SCC 1.

Disallowed cost

Disallowed cost is new to NEC4 PSC and defined in a way similar to that in the ECC. The definition needs close attention, but two key elements are costs, ‘not justified by the Consultant’s accounts and records’, and those, ‘incurred only because the Consultant did not … give an early warning which the contract required it to give’. These are two simple drivers for the consultant to keep good records and do what it says in the contract.

Tendering considerations

Clearly the tenderer has two separate percentages to provide in its NEC4 PSC option C or E tender: the overhead percentage that is only applied to the defined cost of ‘people items’; and the fee percentage applied to all defined cost (see Figure 1 (b)). Once tendered, these percentages would not be subject to audit. For some actual costs it might not be obvious whether they should be covered by the overhead percentage or the fee percentage.

However, when bidding, it is logical for the bidder to set the fee percentage based on the mark-up they wish to receive on subcontractors They will then set the overhead percentage to ensure that their required mark-up on real cost of people is achieved. This would consider whether and which expenses are allowed and that the defined cost of people and the amount for the charge for support people and office overhead costs are subject to the fee percentage. Within those percentages the consultant will also have to make allowances for disallowed cost. In the tender document the client should make clear how it is going to take these percentages into account in tender evaluation.

Conclusions

Before deciding to go along with NEC4 PSC ideas for cost in options C and E, the client must first make sure it understands them and the implication on the resource requirement to verify and audit the costs properly.

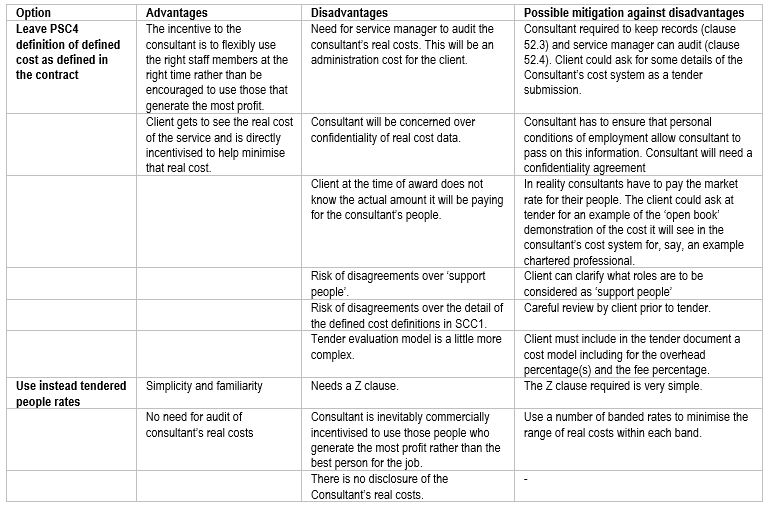

If a client was to choose to revert to rates as were used in NEC3 PSC instead, it would only have to include a Z clause to change the definition of defined cost to that used in option A, copy across the definition of People Rates from Option A, include in contract data part two entries relating to the overhead percentage. It will also have to modify and possibly delete the provision for disallowed cost. Table 2 sets out some pros and cons to consider before making the decision.

For the authors, the main issue with using the NEC4 PSC’s new model is the driver for the flexible use of the right staff at the right time set against the marginal cost of having to audit the consultant’s costs. It will be interesting to see how many clients move to use NEC4 PSC but then revert to rates for the consultant’s people, and how many embrace the open-book approach.

- Table 1. How PSC4 handles money (tendered prices, rates and percentages are highlighted in red)

- Table 2. Advantages and disadvantages of the approach to cost

- Figure 1. Defined cost and expenses in PSC4 option A (a) and options C and E (b), tendered items shown in red

Key Points

- Under options C and E of the NEC4 Professional Service Contract (target and reimbursable options), consultants are paid the real costs of employing staff rather than tendered rates, as was the case in NEC3 PSC.

- Clients need to ensure they fully understand the change and recognise the requirement to audit and verify the consultant’s staff costs.

- Should clients wish to revert to rates, they can do so with simple Z clauses and minor changes to the contract data part two.

- There are advantages and disadvantages to either option.

- Author

- Richard Patterson, Mark Anders and Petter Siljehag - Mott MacDonald

- Share this page

-

- Copy link

{kind=link}

{kind=link}

{kind=link}